Skip to content

Skip to content

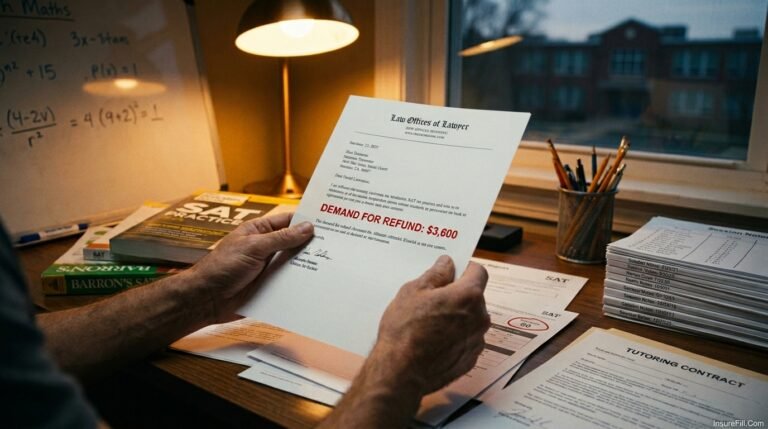

A client invests $18,000 in a paid ads campaign you managed. The campaign underperforms. They blame your strategy. They hire an attorney and send a demand letter. Whether your work was actually negligent or not doesn’t matter yet — your legal defense starts now, and it isn’t free.

Errors and Omissions insurance is the coverage that protects digital marketing consultants from the financial consequences of professional liability claims. In 2026, as clients increasingly require proof of coverage before signing contracts, understanding this protection isn’t optional anymore.

This guide covers exactly what E&O covers, what it costs, which providers offer the best value for consultants in 2026, and how to build a policy structure that matches your actual risk exposure.

What Errors and Omissions Insurance Is

Errors and Omissions (E&O) insurance — also called professional liability insurance — covers you when a client claims your professional advice, services, or work caused them measurable financial harm.

An error is something you did that you shouldn’t have. An omission is something you failed to do that you should have. Both create liability exposure. A general liability policy doesn’t cover either — it covers physical incidents like bodily injury and property damage. E&O fills the gap between what GL covers and the actual nature of professional service work.

According to Hiscox, professional liability insurance is necessary protection against claims that a professional did something they shouldn’t have or didn’t do something they should have while providing services. A general liability policy does not cover these claims — they require dedicated E&O coverage.

How E&O Differs From General Liability

Many consultants confuse these two coverage types because they’re often sold together. They cover fundamentally different risks.

| Coverage Type | What It Covers | What It Doesn’t Cover |

|---|---|---|

| Errors & Omissions | Professional mistakes, bad advice, missed deliverables, negligent strategy | Physical injuries, property damage |

| General Liability | Third-party bodily injury, property damage, advertising injury | Professional negligence claims |

| Combined (BOP + E&O) | Full protection for most consulting scenarios | Intentional acts, criminal activity |

If a client trips in your office, general liability responds. If a client claims your SEO strategy cost them $30,000 in lost traffic, E&O responds. As a digital marketing consultant, you need both — but E&O is directly relevant to the work you do every day.

Why Digital Marketing Consultants Face Higher E&O Risk Than They Realize

E&O claims don’t always come from actual errors. Sometimes they originate from misunderstood expectations, unclear contracts, or a client who is unhappy with results regardless of what caused them.

Digital marketing is particularly exposed to this dynamic because:

- Results are directly measurable — clients can point to specific numbers, making disputes concrete rather than abstract

- ROI expectations are often unrealistic at contract signing — clients frequently expect guaranteed results that no ethical marketer can promise

- Performance depends on factors outside your control — algorithm changes, competitor activity, market shifts, and platform policy updates all affect campaigns

- Deliverables can be vague unless contracts are drafted with extreme specificity

According to the American Marketing Association, disputes between clients and marketing service providers frequently center on performance guarantees and deliverable definitions — the two areas where digital consultants face the most consistent exposure.

What makes coverage essential in 2026 is that clients are now routinely requiring it. Many enterprise companies include proof of E&O insurance in their standard freelance contracts. Some platforms won’t let you list services at all without documented coverage. It’s increasingly the price of admission to professional digital marketing work.

Real Scenarios Where E&O Claims Happen to Good Consultants

Scenario 1 — Algorithm Update You manage SEO for an e-commerce client. Google releases a core algorithm update and their organic rankings drop 40% within two weeks. You didn’t cause the update. You couldn’t have predicted its timing. The client claims your strategy was negligent and files a claim for $22,000 in lost revenue.

Scenario 2 — Unlicensed Image Use You run a social media campaign and use an image that wasn’t properly licensed. The photographer’s attorney contacts your client with a copyright infringement claim. Your client turns around and sues you for the damage caused.

Scenario 3 — Missed Launch Deadline A campaign launch is delayed one week due to an approval miscommunication. The client calculates $8,000 in losses from the delay window and files a formal claim against you.

Scenario 4 — Budget Misallocation You advise a client to shift budget toward YouTube from search. The channel underperforms. They claim your advice was negligent and that you should have known the channel wasn’t appropriate for their audience.

None of these require incompetence. Every one of these has happened to experienced, qualified marketing professionals.

What E&O Insurance Covers for Digital Marketing Consultants

A solid E&O policy for consultants typically covers:

Professional Negligence Claims — If a client alleges your advice, strategy, or execution fell below professional standards, the policy covers legal defense costs and any judgment or settlement up to your policy limit.

Defense Costs — Even completely frivolous claims require a lawyer to respond. E&O policies cover attorney fees, court costs, and expert witness fees. This alone can reach tens of thousands of dollars before a case resolves.

Errors in Deliverables — If a report you produced contained incorrect analytics data that led to bad business decisions, or if your tracking setup measured the wrong metrics for months, that’s a covered claim.

Omissions — Missing a step in a campaign setup, failing to disclose something material, or omitting a key element from a deliverable all fall under E&O coverage.

Violation of Good Faith — If a client claims you didn’t act in their best professional interest during the engagement, this allegation typically falls under E&O.

What E&O does NOT cover:

- Intentional fraud or criminal acts

- Bodily injury or property damage (general liability handles those)

- Employment-related disputes between you and your staff (requires EPLI)

- Claims from work done before your policy’s retroactive date

- Breach of contract claims in some policy structures — read your policy specifically

How Much Does E&O Insurance Cost for Digital Marketing Consultants in 2026?

E&O insurance is far more affordable than most consultants assume until they actually get a quote.

According to constructioncoverage.com’s March 2026 analysis, Hiscox advertises E&O policies starting as low as $22.50 per month (approximately $270 per year) for qualifying small businesses, with rates that scale based on business type and size, according to Construction Coverage’s March 2026 analysis. The Hartford reports average E&O costs ranging from $500 to $1,000 per employee per year for professional services firms.

| Business Size | Annual Premium Range | Typical Coverage Limit |

|---|---|---|

| Solo Consultant | $270 – $1,200/year | $1M per occurrence |

| Small Agency (2–5 people) | $1,200 – $3,500/year | $1M – $2M per occurrence |

| Mid-size Agency (6–20 people) | $3,500 – $9,000/year | $2M – $5M per occurrence |

These are industry averages based on data from Insureon, NEXT Insurance, and Hiscox, which regularly publish small business insurance cost data for professional services roles.

Factors affecting your individual premium:

- Annual revenue — higher revenue means broader exposure, which increases premium

- Years in business — experienced consultants with clean records often qualify for better rates

- Services offered — managing large paid media budgets carries more exposure than organic social

- Claims history — a first-time buyer with no prior claims qualifies for the lowest tier

- Deductible and limits selected — adjusting these directly affects cost

- Location — states with higher litigation rates generate higher premiums

One legal defense case costs $50,000 or more even if it never reaches a verdict. Monthly premiums for solo consultants are typically less than most spend on software subscriptions. That ratio is the strongest argument for coverage.

Top E&O Insurance Providers for Digital Marketing Consultants in 2026

According to MoneyGeek’s April 2026 professional liability rankings, the top three E&O providers nationally for professional services firms are The Hartford, Hiscox, and NEXT Insurance — rated on coverage quality, price, claims handling, and industry specialization in MoneyGeek’s April 2026 rankings.

| Provider | Best For | Key Feature |

|---|---|---|

| Hiscox | Solo consultants and small agencies | Covers 180+ industries, policies from $22.50/month, worldwide work coverage |

| The Hartford | Mid-size agencies | Strong bundling with Business Owner’s Policy |

| NEXT Insurance | Fast coverage | Digital-first, same-day coverage, 100% online |

| Insureon | Comparing multiple quotes | Marketplace model for carrier comparison |

| Simply Business | Flexible options | Monthly payment, easy to adjust coverage mid-term |

Always get at least three quotes before deciding. Coverage terms — especially around retroactive dates and defense cost structures — matter as much as the premium.

Policy Features That Make a Real Difference

Claims-made vs. occurrence-based. Most E&O policies are claims-made — the policy must be active both when the alleged incident happened and when the claim is filed. If a project ends in 2025 but the client files in 2027, you need an active policy or tail coverage in 2027. Occurrence-based policies cover incidents during the policy period regardless of when claims arrive — harder to find for professional liability but stronger protection.

Retroactive date. Your policy’s retroactive date determines coverage reach. A retroactive date of January 2024 means claims from work before that date aren’t covered. Push for the earliest possible retroactive date — ideally back to when you started your consulting practice.

Defense costs inside vs. outside limits. Policies that pay defense costs on top of your coverage limit (“defense outside the limit”) are substantially better. Legal fees won’t eat into your available settlement coverage.

Worldwide work coverage. Hiscox professional liability policies cover work performed worldwide, as long as any legal action is filed in the U.S., U.S. territories, or Canada. If you work with international clients, confirm your policy includes this.

Your consent before settlement. Quality policies require your explicit approval before the insurer settles. This protects your professional reputation, not just your balance sheet.

E&O coverage works best as part of a complete protection strategy. For consultants managing client data through CRM systems, analytics platforms, and email lists, cyber liability coverage matters alongside E&O. The personal cyber liability insurance guide covers how digital risk coverage complements professional liability for knowledge-based freelancers. For content-producing consultants, the brand defamation insurance guide explains how media liability fits into broader digital risk protection.

How E&O Insurance and Client Contracts Work Together

Insurance is one protection layer. Strong contracts are another — and they work better together than either does alone.

Your client contracts should include:

- Scope of work with explicit exclusions. State exactly what you will deliver and specifically what falls outside the engagement. “We will manage Google Ads campaigns for budget up to $10,000/month” is better than “we will handle paid advertising.” If SEO isn’t included, say so explicitly.

- Performance disclaimers. State clearly that campaign results depend on multiple factors outside your control — platform algorithm changes, competitor activity, market conditions, and client-side variables including product quality, pricing, and fulfillment. Protecting yourself from result-based claims starts with setting accurate expectations in writing.

- Limitation of liability clause. Cap your total financial liability to a defined amount — typically the total fees paid for the specific engagement or one month’s retainer. This doesn’t prevent claims, but it limits your worst-case exposure.

- Revision and approval process. Specify how many revisions are included, what the approval process is, and who has final sign-off authority. Disputes about whether deliverables were approved are among the most common triggers for E&O claims in creative and marketing work.

- Dispute resolution clause. Require mediation or arbitration before litigation. This keeps disputes out of court, which dramatically reduces costs for both parties.

Combining precise contracts with proper E&O coverage is the professional standard in 2026. One without the other creates gaps that the other can’t fully compensate for.

Documentation Practices That Help at Claim Time

Good documentation habits cost nothing and pay significant dividends if a claim arrives.

Keep written records of all major decisions: when a client approved a campaign direction, when a budget was confirmed, when a deliverable was signed off. Don’t rely on verbal conversations. Follow up key calls with an email summary: “As discussed today, we’re moving forward with X approach and budget Y — please confirm.”

Save all client feedback and revision requests in writing. If a client later claims you ignored their direction, your documented record of their actual requests is your defense.

Store project files, analytics reports, and deliverables for a minimum of three years after a project closes. Professional liability claims sometimes arrive long after an engagement ends.

Understanding Claims-Made Policy Mechanics in Practice

Most digital marketing consultants have never had to think about the difference between claims-made and occurrence-based insurance. But if you ever switch providers or cancel coverage, these mechanics determine whether your prior work remains protected.

The basic claims-made rule: Your policy must be active both when the professional act occurred and when the client files the claim. If you ran campaigns for a client in 2024, let your policy lapse in 2025, and that client files a claim in 2026 — you have no coverage.

What tail coverage does: Tail coverage — formally called an Extended Reporting Period (ERP) endorsement — is an add-on you purchase when canceling a claims-made policy. It allows you to report claims during the tail period for incidents that occurred while your policy was active. Standard tail periods run 12, 24, or 36 months. The cost typically runs 100–300% of your annual premium as a one-time payment.

Why this matters for switching insurers: If you find a better E&O policy at renewal, don’t cancel your existing policy before confirming the new one is active. A gap in coverage — even a single day — can leave prior work unprotected.

Retroactive date management: When switching insurers, ensure your new policy’s retroactive date is set no later than your original policy’s inception date. Some carriers try to set retroactive dates to the new policy start, which removes coverage for all prior work. Negotiate this before signing.

According to the NAIC, policyholders have the right to request specific policy terms including retroactive dates — and should document any verbal agreements about coverage scope in writing before a policy binds, according to the National Association of Insurance Commissioners.

Working With Subcontractors and Freelancers

Many digital marketing consultants bring in subcontractors — copywriters, designers, media buyers, developers — for specific project needs. This creates a coverage question worth addressing directly.

Your E&O policy may or may not extend to work performed by subcontractors on your behalf. Policies vary on this point. Some treat subcontractors’ work as covered under your policy when they’re working under your direction. Others explicitly exclude subcontractor-related claims or require each subcontractor to carry their own coverage.

Best practice: require all subcontractors to carry their own E&O insurance and name you as an additional insured where possible. This creates a second layer of protection. If a subcontractor’s error generates a claim, their policy responds first — yours serves as backstop if needed.

For freelancers who also provide knowledge-based services across multiple disciplines — tutoring, consulting, virtual assistance — understanding how E&O structures work in parallel service offerings matters. Our freelance tutors’ indemnity insurance guide covers the E&O decision framework for knowledge-based independent workers in educational services.

When Clients Ask for Proof of Insurance

In 2026, requesting a Certificate of Insurance (COI) before signing is standard practice for enterprise and mid-market clients.

Getting your COI. When a client asks for proof of coverage, your insurer generates a one-page Certificate of Insurance summarizing your policy. Most carriers provide this digitally, often within minutes of requesting.

Additional insured endorsements. Some clients request to be listed as an “additional insured” on your policy. Not all E&O policies support this — confirm with your provider before promising it.

Minimum coverage requirements. Enterprise clients often specify minimums — typically $1M or $2M per occurrence. Know your limits before pitching to large accounts.

Frequently Asked Questions

In most cases, no legal mandate exists. However, many corporate clients contractually require it before signing, and some platforms require it to list services. The financial exposure without it — even one defense case can cost $50,000+ — makes it functionally essential for any consultant working at professional rates.

It depends on your policy. Some extend coverage to subcontractors working under your direction. Others exclude them entirely. Read your policy carefully and ask your provider directly. Subcontractors not covered by your policy should carry their own E&O coverage.

The retroactive date determines when your coverage begins looking backward — no coverage for work done before that date. Tail coverage is an add-on that lets you report claims after your policy ends for incidents that occurred during active coverage. If you ever cancel your E&O policy, purchasing tail coverage is strongly advisable.

NEXT Insurance and Insureon can often bind a policy within hours of completing an online application. Same-day coverage is genuinely available for solo consultants. If a client needs a Certificate of Insurance urgently before a project start, this timeline is achievable with most major providers.

Yes. Providers evaluate projected revenue and work type, not past client volume. Starting with coverage from day one means your retroactive date is maximally useful and you’re protected immediately when you acquire your first client.

Standard E&O policies don’t automatically cover copyright or trademark infringement — these typically require a media liability endorsement. If you regularly create content, design assets, or use third-party media in your work, review your policy’s intellectual property terms specifically.